A Committee to Save the Rest of the World

Trump’s trade policies could impose severe damage on the international economic order. The rest of the world should get organized to limit the damage.

[Note: this is a more elaborate version of a comment I did for the Hinrich Foundation. Do read that one if you like shorter pieces!]

The first months of the second Trump administration has been a wild ride. On day one, Trump announced disengagement from the Paris Agreement and the WHO, and ordered a review of US engagement in all international organizations including IMF and World Bank. The US also opted out of the G-20 this year, slashed commitment to international development, withdrew major support for Ukraine in their fight against Russia’s invasion, and . The US has also imposed tariffs on its closest trade partners Canada and Mexico, and threatened them against its allies the EU, Korea, and Japan as well as the rest of the world. The Wall Street Journal editorial page, a vanguard of conservatism, called it The Dumbest Trade War in History.

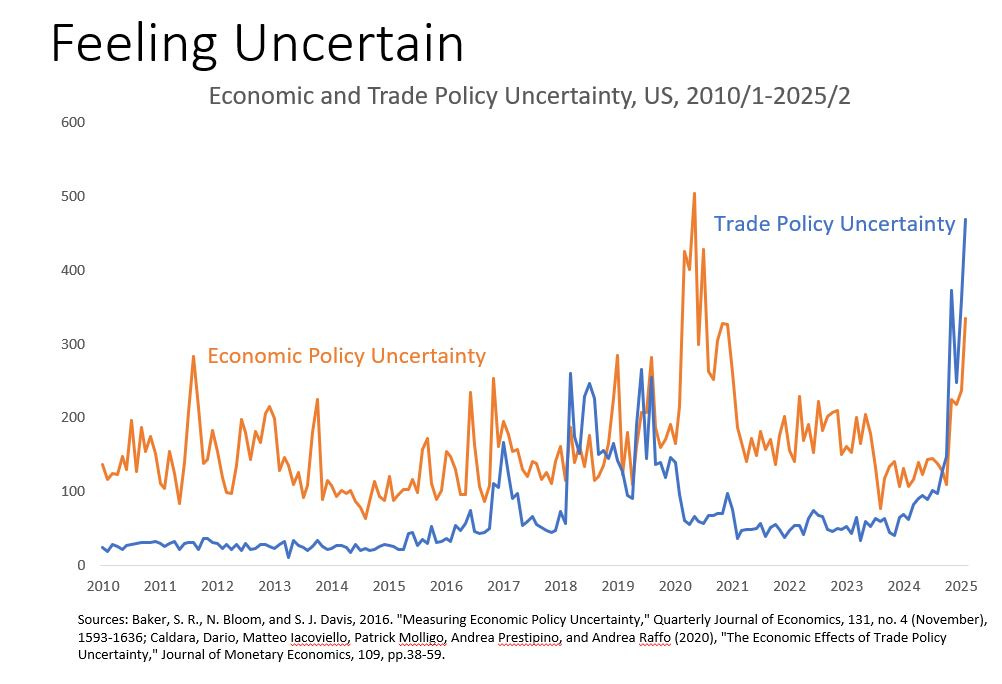

Part of the damage is already done. Trade policy uncertainty is at historic highs, and overall policy uncertainty is not far behind. Stock markets in the US reacted sharply negative, the dollar weakened, and consumer confidence took a plunge. This uncertainty has real consequences: investors take a wait and see attitude, and consumers postpone large acquisitions of consumer durables and housing. Goldman Sachs estimated that trade policy uncertainty alone could cost the US some 0.3 percent growth this year, and more for those countries heavily dependent on exports to the US. This has started to show in downward revisions of economic growth projections of investment banks. The IMF and World Bank both see a trade war as a major downside risk to their economic projections. A full-blown trade war could cost as much as 7 percent of global GDP according to IMF scenarios. Unimaginable only months ago, there is now talk of a recession in the US.

The turmoil in recent weeks is only the start of Mr. Trump’s policy agenda. His America First Trade Policy, announced by executive order on his first day in office is to be the basis for “reciprocal tariffs,” after April 1. The executive order is conceptually flawed. A trade deficit is not a “subsidy” by the US to other countries, tariffs don’t reduce the overall trade deficit of the US, and don’t bring back industries—as Trump 1 has demonstrated. Most annoyingly, a Value Added Tax, levied by many governments around the world, is not a tariff, and is levied equally on domestic and foreign producers. Sadly, these flaws in the arguments are unlikely to prevent the imposition of more tariffs.

Less visible is the America First Investment Policy. The policy is largely aimed at investments to and from “China and other adversaries” squarely puts national security at the center of economic policy: “Economic security is national security” is a line that is not dissimilar to Xi Jinping’s words “National security is the bedrock of national rejuvenation” spoken at the 20th national party congress of the communist party of China. The executive order largely reiterates existing policies such as CFIUS and the US Outbound Investment Security Program, but expands the coverage of both. It also breaks new grounds on investment of US citizens in Chinese companies, or companies outside China with Chinese connections (such as Tiktok, a Singapore company with Chinese owners). The executive order shows an obsession with Chinese ownership of agricultural land—China holds about 1 percent of total foreign owned farmland, or less than 0.05 percent of total farmland in the US.

The Chaos is the Plan

In Mr. Trump’s first term, much the threats in the end did not become policy. There is less hope for that in his second term, though, as no traditional Republicans, a source of moderation during Trump 1, are in the cabinet room now. Mr. Trump’s thoughts on trade are deep seated, and have formed in the 1980s when Japan (and Saudi Arabia) was his bogeyman. He famously took out a full page add in the New York Times to declare that “for decades Japan and other nations have been taken advantage of the United States.” The solution? Tariffs, of course. “Tariffs is the most beautiful world in the dictionary” Mr. Trump told Bloomberg last year. The real agenda may be far broader than trade: If it succeeds, it may profoundly upend the international order it led to create after World War II.

There are talks of a “Mar-a-Lago Accord” that would make the world whole again, in the minds of the Trump team. Such an Accord would be a “reset” of the world of international finance and trade with the spoils accruing to the US. Disruption, in this thinking, is part of the plan as penned down in October last year by Steven Miran, Trump’s pick for heading the Council of Economic Advisors. For now, it is just talk, and the US seems to be the only party really interested in such a grand bargain. The memories of the Plaza and Louvre Accords are still fresh on the mind of the Japanese and China has studied the Accords in-depth. they are not interested, even though they see some merit in “major power diplomacy,” which Xi Jinping proposed to Obama at the Sunnylands summit in 2013. The US subsequently passed on the notion, as it felt it would benefit the Chinese more than the US.

What should be done?

“In a crisis we have to focus on what we can control” said Mark Carney, the new Prime Minister of Canada during his campaign. This is first and foremost the domestic agenda.

Europe has the biggest challenge, as they will need to change their security agenda and their economic agenda at the same time. Fortunately, they have a plan that does both—the Draghi plan. The plan, presented in September last year, aims to make the EU more innovative, greener, and more secure. Mr. Trump’s talk on NATO and actions vis-à-vis Ukraine has intensified concerns on the US as a reliable partner, and have given this agenda urgency, and major countries in Europe have realized this, and are preparing to move. If they achieve more research and development, deeper integration of the European market, and more autonomy in defense, the MAGA agenda could achieve a stronger and more autonomous Europe over time.

China has had its own agenda for almost a decade. Its “new development philosophy” introduced in 2015 aims for higher quality growth, boosted by productivity increases and innovation. Last year’s Party Plenum finally put more meat on what this would mean. Though a work in progress, China’s manufacturing might and innovative firms such as BYD, Huawei, Alibaba and Deepseek signal that this is a viable direction and that China is likely to succeed. What is lacking thus far is sufficient domestic demand: if Mr. Trump pushes through his campaign promise of 60 percent tariffs, this could cost some 2-2.5 percent of GDP, which domestic demand would need to make up for. Failing that, China’s surpluses with the rest of the world will increase further, adding tensions to the international trading system.

In south-east Asia, the unfinished agenda of the ASEAN economic community offers the best chance to counter the negative fall-out form Trump-2. Some ASEAN countries were winner from Trump 1’s trade policies as they became connectors between Chinese exports and US imports. China has also started to invest more in manufacturing in the region, even though the US, Japan and EU remain larger investors. ASEAN’s luck is unlikely to last under Trump 2: the America First Trade agenda would punish those that did well from this arrangement. So, like the EU, ASEAN integration has become ever more important, and not just to better absorb Trump’s trade measures, but also to maximize the benefits from the growing presence of Chinese investment and renewed EU interest in the region.

The international agenda.

As important as the domestic agenda is the international one. Countries are individually less in control, but neglecting that part of the agenda risks that Trump’s agenda becomes the international agenda by default. Take electric vehicles, a sector in which China is the leading producer and exporter. Because the US levies a prohibitive 100 percent tariff on Chinese vehicles, exports are largely directed to other markets, including Europe, which in turn imposed tariffs on its own. Such a side-effect, if generalized, could turn US trade policy into a global trade war.

There are plenty of options for countries to pursue a different course of action:

First, responding to Mr. Trump’s tariff threats. Tit-for-tat tariffs may be unavoidable in negotiations, as Mr. Trump would see the absence of a response as weakness and an invitation for more abuse. Nevertheless, the optimal response to tariffs would be to subsidize the affected sector, and lower tariffs for everybody else. Affected countries could as a minimum agree not to further aggravate the impact on the world economy, and agree on a coordinated lowering of tariffs on all other imports, thereby effectively containing its overall tariffs levels.

Second, deepening of trade ties. The existing trade agreements in Asia could be deepened, and expanded. RCEP, the largest agreement in terms of the GDP of its member countries, could be deepened, and broadened with new members. China could double down on its efforts to become a member of the more ambitious CPTPP agreement, which would spur domestic reforms in China and productivity in all members., and set limits to state support to companies, one of the most contentious issue in international trade. Even re-upping the Comprehensive Agreement on Investment between the EU and China should be on the table again, though, diplomatically, perhaps under a different name. The agreement was derailed in 2021 after the EU sanctioned China for alleged human rights abuse in Xinjiang, and retaliation by China. Now would be a good time to table the agreement again, and strengthen ties between the two largest trading blocks in the world.

Third preserving the multilateral system. While the WTO mechanism is incapacitated because of the US has been blocking appointments of appellate body judges, it should still be the defence of choice against the Trump Tariffs. Using the WTO, such as China has consistently done, maintains the legitimacy of the organization, and reinforces the commitment to multilateral channels. And although the US has not signed up, the Multi-Party Interim Appeal Arbitration Arrangement can safeguard the rule-based trading system in the interim.

Fourth, thinking the unthinkable. Though the odds on a US withdrawal from core global institutions such as the IMF and World Bank and others, Project 2025 prescribes exactly that. Rather than wait for such a calamity to happen. Until now, much of the thinking has been focused on how the international monetary system could gradually adjust to a rising China (and India). Much more radical reforms may be needed if the leader of that system decides to call it quits.

The Committee to Save the Rest of the World.

The pursuit of this international agenda requires leadership. Leadership is a global public good, which with the sudden pivot of the US to an America First agenda, is in short supply. The world finds itself acutely into a “Kindleberger trap. The concept, introduced by Joseph Nye, is based on Charles Kindleberger’s observation that after World War 1 the UK was no longer capable of providing global public goods, whereas the rising power, the US at the time, was reluctant to do so. The result was the disastrous 1930s, with the international monetary system in tatters, a beggar thy neighbor trade policy, and ultimately was. This experience was a key motivation for the architects of the post-WWII international order. Now the lead architect no longer supports the system. Someone else should.

Time Magazine’s cover of February 15 famously presented the “Committee to Save the World.” It showed a picture of US treasury secretary Robert Rubin, Fed Chairman Alan Greenspan and US Undersecretary of the Treasury Lawrence Summers. The cover reflected the mood at the time: the three Americans had been fighting crises around the world, from the 1994 Tequila Crisis to the Asian Financial Crisis and the Russian subnational default. While their prescriptions to contain the crises are debated until this day, there was no doubt that the US played a central role in coordinating the world’s response to the crises in the international financial system.

Now that the US itself has become the disruptor of the international economic system, a de facto a multilateral world is emerging. That is still a world that needs to be steered and led. A Committee to Save the Rest of the World could coordinate a multilateral the response to the unilateral Trump agenda, and prevent a repeat of the history of the 1930s. Now is the time for “coalitions of the willing,” minilateral or plurilateral groups to sit down and work on joint responses, or at least coordinated ones.

Who exactly should be on the committee remains to be seen, but a natural one that rose to prominence after the global financial crisis is the G-20—or G-19 for now. The G-20 has lost some of its luster since, and recent geopolitical events have not been kind to the platform. The US’s decision to forego this year’s G-20 is an unexpected opportunity for the rest for the rest of the world to get organized. If the G-19 can manage to focus on economic issues this year, the world stands a chance to limit the fallout from Trump’s economic agenda.

Thanks for the comprehensive review. You don’t see a role for BRICS? And China’s BRI?