The Economic Consequences of a new Cold War

The economic costs of a new cold war would be disastrous, but unavoidable without rebuilding trust.

In his latest tour to Europe this May, China’s minister of foreign affairs Qin Gang was on a mission. He had a clear aim: to prevent Europe joining the US in its endeavour to limit China’s access to advanced technology. He called on his German counterpart to “stick to the right path, jointly oppose the new Cold War, and decoupling economies or severing supply chains.” He faces an uphill struggle.

European Commission President Ursula von der Leyen, in a hawkish speech on April 20, had assured China that the EU did not seek to decouple from China, but that it wants to “de-risk” the relationship. What that means is set to become clear in the coming weeks, when the EU is to present a list of goods and technologies that are too risky to hand to China.

US Secretary Yellen had struck a similar tone in a speech at Johns Hopkins University. She said that the first principal objective of the US economic approach to China is to secure national interests. She added that the US is also seeking a healthy economic relationship with a China that “plays by the rules,” and continued to seek cooperation on global issues such as climate change.

US National Security Advisor Jake Sullivan sang from the same hymnbook as Yellen a few days later at the Brookings Institute. He spoke of restrictions on a limited slice of technology, of “small yards with high fences.” Sullivan’s tone had mellowed from that of a speech last September ahead of the announcement of US export restrictions on semiconductors to China, which put the US aim as keeping absolute advantage over China in critical technologies.

That aim has not changed. Since the US export ban took effect last October, the Netherlands and Japan were politely asked to join the US efforts on semiconductors, as they are critical suppliers in the industry. It was an offer they could not refuse.

Meanwhile, the US CHIPS Act and the Inflation Reduction Act put money towards the aim of reducing dependence on other countries for critical technology, including semiconductors but also renewable energy. In turn, the EU has doubled down on its industrial policy initiatives on Digital Europe and Green Europe. Like the US, European countries have in recent years tightened national security reviews of Chinese investment, and together with the US, they have set up a Technology and Trade Council to coordinate tech and trade issues.

The Age of Geo-economics

Despite the occasional clashes between the EU and the US on the protectionist impact of these measures—and these are abundant—the two blocks seem to converge on a trade and investment policy that aims to de-risk their relationship with China. “The United States and the European Union are working to reinforce, through transatlantic cooperation, our essential security interests and the resilience of our economies…..We are increasing our cooperation to prevent the leakage of sensitive emerging technologies, as well as other dual-use items, to destinations of concern that operate civil-military fusion strategies” the joint statement of Von der Leyen’s visit the White house read. Translation: China. “The New Washington Consensus” Edward Luce of the Financial Times called it.

China is of course no stranger to an industrial policy driven by national security concerns. The Communist Party of China (CPC) General Secretary has throughout his past two terms emphasized national security as key concern. The strive for “indigenous innovation” has aimed at reducing dependence on foreigners for critical technologies, with mixed success. China’s “dual circulation” strategy is, as Xi Jinping explained, aimed at reducing dependence on other countries in critical supply chains, while encouraging the dependence of other countries on China. At the 20th Party Congress general secretary Xi expressed it clearly “National security is the bedrock of national rejuvenation, and social stability is a prerequisite for building a strong and prosperous China.” The 14th Five Year Plan (2021-25) puts topics such as food security, energy security and indigenous innovation at the top of the list.

China’s negative list for foreign investment in part reflects national security concerns as well. China’s cybersecurity law, which regulates data transfer across borders, and more recently the expansions of the definition of espionage are further complicating doing business in China for foreign companies. The recent police raids of the offices of several due diligence companies have poured cold water on the prospects of foreign investors, which rely on such companies to ensure their suppliers or acquisitions abide by their standards (note, however, the recent Sinica Podcast on the -Chinese-firm Capvision).

Despite its stated objection against unilateral sanctions, China has bene using economic instruments for achieving international political means as well. This usually affects China’s imports from countries it has a disagreement with, but it has also used exports controls in the case of the dispute with Japan over the Senkaku/Diayu islands. The COVID-19 pandemic put into focus the high dependence many countries had on production from China, from medical gear to medicine to rare earths and batteries for electronic vehicles. The renewed enthusiasm for industrial policy in the EU and the US can at least in part be understood as a means to reduce dependency in supplies from China.

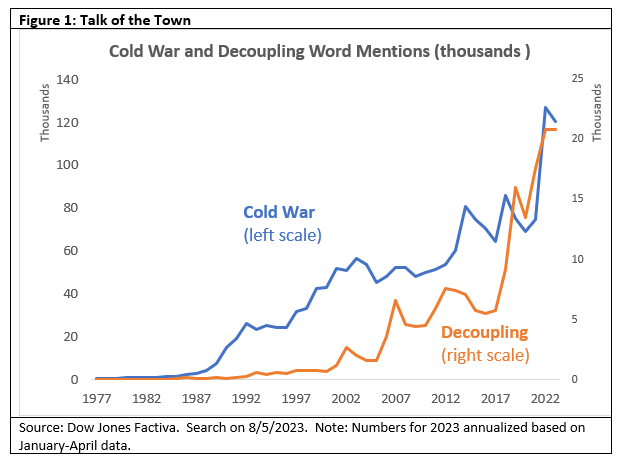

The growing geopolitical tensions between China, The United States and Europe have given rise to a whole new vocabulary. National security, decoupling, de-risking, onshoring, friend-shoring, near-shoring, and Cold War II are now the talk of the town, a simple search for those terms will tell you (Figure 1).

Geopolitics is reshaping the global economy, and will do some for the foreseeable future. We have indeed entered an era of “geo-economics.” Depending how the balance of national security and economy is struck in the end, the damage can be considerable, and even catastrophic.

Not your grandfather’s cold war

A new cold war, if it ends that way, will be very different from the last one. The Soviet Union and its COMECON allies hardly had any interaction with the west, and even that was focused on commodities, such as the grain-for-oil deals between the USSR and the United States. Trade with the USSR never amounted to more than 2 percent of the OECD’s total trade.

In contrast, China today is a key note in global supply chains, supplies some 20 percent of imports of advanced economies, and is increasingly a supplier of intermediaries to other countries, notably in South East Asia. This means that global supply chains increasingly depend on inputs from China, from rare earths to batteries to machine tools.

Furthermore, China is becoming more and more a source new technologies, innovation and ideas, produced by the millions of STEM students graduating every year, and the hundreds of thousands of PhDs, many of them studying and working at universities in the west. In peaceful times, this is a source of great benefits to the world, but in times of tension it is seen as a worrisome gain in capacity of a potential adversary.

The end of the first cold war also meant a large “peace dividend” of reduced spending on the military. According to numbers of Stockholm-based SIPRI, military spending as a share of global GDP fell from 6 percent of global output in the 1960s at the peak of the cold war to 2.1 percent in 20221. The same national security concerns that are reshaping global value chains could lead to increased military spending.

Gradually, though, companies around the world are starting to adjust to the new geopolitical landscape, and investment by investment, trade deal by trade deal, this is reshaping the global value chains. Strategies such as a “China+1” “China for China” and a more general diversification strategy to reduce dependence on China as a client are debated in Boardrooms around the world. The impact of the US restrictions on technology transfer—current, and potentially future—is increasingly playing a role in this strategic calculus, and with it the shape of global supply chains is changing.

The benefits of globalization

Globalization was driven by three things: technology, trade policy and politics. The invention of transport containers in the 1950s revolutionized international trade, first gradually, and then quickly as port facilities around the world adapted to the new phenomenon. The major improvements in communication technologies from the 1990s made outsourcing and offshoring cheaper and easier to manage, which enabled a jump in FDI and more rapid diffusion of technology across the globe.

Second, the gradual reduction in trade tariffs, first under the General Agreement on Tariffs and Trade, and then at the establishment of the World Trade Organization in 1996 reduced the costs of trade significantly. With it came the opportunity to produce not just goods, but individual parts of goods in the country that could do so best, or cheapest. Global value chains emerged in which parts of goods crossed borders more than once before reaching final demand.

Third, the end of the Cold War meant that more than a billion workers in China, Vietnam, the Former Soviet Union, and Eastern Europe joined the global economy. India’s reforms of the early 1990s added another large economy to this, even though the country’s integration in the world economy is less than that of China’s.

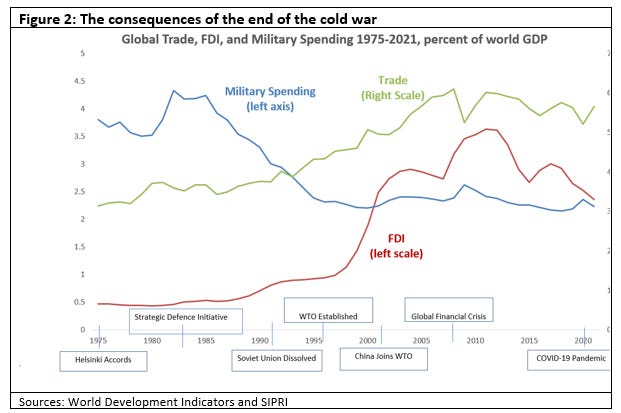

Together, these three forces drove global trade, growth and productivity in the past 5 decades (Figure 2). Trade as a share of global GDP more than doubled from 25 percent in 1960 to 56 percent now. Foreign Direct Investment (FDI) quintupled from about half a percent of GDP in the 1960s to an average of about 2.5 percent of GDP in the past decade. Import tariffs across the world were slashed from 8.5 percent on average before the WTO to 2.6 percent now. Remarkably, growth in global income per capita in the 20 years after WTO was almost 50 percent higher than of the 20 years before it, even though it was lower in advanced countries, and about the same in China.

The global financial crisis heralded the end of hyper-globalization. Discontent with the domestic distributions of the gains, and concerns on environmental consequences and vulnerability to shocks have driven a rethinking of globalization. Since the GFC, global trade as a share of world output has moved sideways, whereas the share of FDI in global GDP went from more than 3 percent in the 2000s to less than 2 in the last decade.

Developments in China played a significant role in this: the country’s growing domestic supply chains meant that more and more of what it previously imported was now produced at home. The growing share of domestically produced parts that go into the i-phone is just one example of this phenomenon. While this can still be understood as a normal outcome of a country that successfully develops, it is also a sign that China’s dual circulation strategy is leaving its marks already.

Signs of things to come

Until recently, and in part due to the disruptions caused by COVID-19, it was hard to detect any geo-economics in the numbers on trade and investment. Now, some signs of decoupling are now visible in the numbers. China’s exports to the US have declined as a share of US imports, and the goods hit by the Trump tariffs have done especially poorly. At the same time, exporters, including Chinese exporters, have adjusted and exports of Viet Nam, Thailand and Vietnam to the US have been thriving. Meanwhile, China’s exports to those countries—of intermediary goods, have sharply increased.

FDI is also showing signs of a realignment. Even though FDI inflows in China are still holding up, much of it comes from established firms reinvesting their profits. The number of new investments is way down though: according to the IMF, the number of greenfield investments from the EU and US into China was down by 20 and 40 percent in 2022 compared to the average of 2015-2021.

The Rhodium Group found that investment of the EU into China is increasingly concentrated among the top-10 investors, companies such as BASF and Volkswagen. Smaller investors stay away, awaiting clarity on how geopolitics will work out. Meanwhile, China’s investment overseas is also down: investments into the United States have practically fried up, and the country invested less than EUR 8 billion in Europe in 2022, less than 1/5th of the number in 2016. Even though the numbers are clouded by the COVID-19 pandemic, exchange of students and academic cooperation between the US and China are also down, signaling decoupling beyond trade and investment.

Damage assessment

Things could get worse. In 2020, the Rhodium Group explored a “Green List” approach for the EU—the same type of list Von der Leyen is now working on. According to that study, some 56% of EU exports to China are completely benign, while 83% of China’s exports to the EU qualify as “green.” FDI vulnerabilities are larger: some 46% of China’s FDI in the EU and 32% of the EU’s FDI in China in 2019 fail to make the Rhodium green list. If representative for the EU approach to come, this would mean significant disruptions ahead in the EU-China economic relationship.

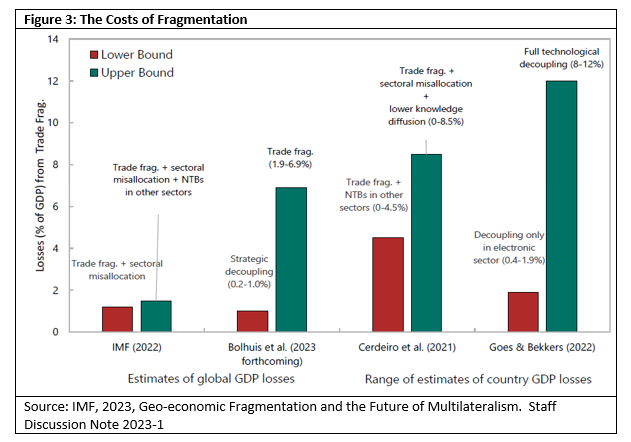

The IMF has recently estimated what a fragmentation of the world economy into economic blocks would imply. According to them, the costs of investment fragmentation could lower global GDP by 1 percent, and double that for GDP in China. Trade and technology fragmentation can be more damaging still: the cost to global output from trade fragmentation could range from 0.2 percent in a limited fragmentation scenario to up to 7 percent of GDP (in a severe fragmentation / high-cost adjustment scenario). With the addition of technological decoupling, the loss in output could reach 8 to 12 percent in some countries.

These are massive costs. To compare, the benefits of Regional Comprehensive Economic partnership, a major trade agreement, are estimated at about 0.6 percent of GDP by the ADB. In a recent report for the UK Department of Trade, academics estimate the benefits of the WTO for the average country at 4 percent of GDP. In other words, losses from geopolitical fragmentation could be two to three times larger than the gains the WTO produced.

Economists are only starting to grapple with decoupling, and until now they have largely used standard models used for trade liberalization. Though these are analytically sound, they tend to underestimate dynamic effects such as productivity gains (or losses) from innovation and competition, and usually disregard the disruption caused by companies and countries adjusting to a new world.

These dynamic costs will be far from trivial. Take innovation. China currently spends some 2.5 percent of GDP on R&D, or some USD 433bn., second only to the United States. China currently already has the largest number of researchers in the world, a number that is rapidly rising. In an integrated world, these would be to the benefit of everybody on the planet, and produce innovations and solutions for today’s challenges. In a decoupled world, these resources could be increasingly diverted to duplication of research and reinvention of the wheel.

All of this still leaves aside a possible upturn in military spending. In the wake of Russia’s invasion of Ukraine, many European NATO members are now considering upping their spending to the NATO norm of 2 percent of GDP, and in addition, Germany has announced a special allocation of EUR100bn. to refurbish their military. Japan has committed to increase its spending to 2 percent of GDP by 2027, an increase of 60 percent. World military spending overall grew by 3.7 percent in real terms in 2022, the highest level ever recorded by SIPRI, which has numbers dating back to 1949.

Irrespective how long green lists are, or how small the yards with high fences without a restoration of some level of trust between the US and Europe on the one hand, and China on the other, as I argued almost 3 years ago. If a country cannot be certain of supplies of critical goods from one country, it will seek to diversify away from the most efficient supplier, and choose an ally to supply it, or reshore production altogether, irrespective of the efficiency losses. If a country cannot be assured of access to critical technologies, it will choose to invent it itself, irrespective of the duplication involved.

Strategic Trust as Vivian Balakrishnan called it recently in a speech at the ANU is the glue that keeps the global order from disintegrating. If a country cannot be reasonably certain that it can import the critical goods and technology it needs, that country will strive to make it itself. This classic prisoners’ dilemma will result in a world of trade blocks, and all will be worse off than today.

"At the same time, exporters, including Chinese exporters, have adjusted and exports of Viet Nam, Thailand and Vietnam to the US have been thriving. Meanwhile, China’s exports to those countries—of intermediary goods, have sharply increased."